Written by Aries Yuangga

Summary

Microsoft (NASDAQ: MSFT) is still one of the highest-quality businesses on the planet, but the story is no longer “zero-risk mega-cap”.

Core engines are on fire:

- Productivity & Business Processes (Office, Teams, LinkedIn)

- Revenue +16% YoY

- Gross profit & operating income both ~+20% YoY

- Intelligent Cloud (Azure + server products)

- Segment +28% YoY

- Azure & other cloud services +40% YoY

- AI demand “exceeded supply” even as capacity ramped

But there are real uncertainties:

- More Personal Computing (Windows, Devices, Xbox) is slowing

- Segment only +4% YoY

- Xbox content & services +1% YoY

- Heavier competition from Valve (Steam + new consoles), Sony, Apple

- Competitive pressure in AI, productivity, and cloud from:

- Google (Gemini, Docs/Sheets, Google Cloud)

- Amazon (AWS)

- Valuation is not cheap at ~30x forward earnings on a $3.6T company.

📌 Thesis: MSFT is still a tier-1 compounder, but buyers today should accept valuation + competitive risk.

📌 Rating: CAUTIOUS BUY, accumulate on dips into the buy zone, don’t chase vertical candles.

Technical Analysis

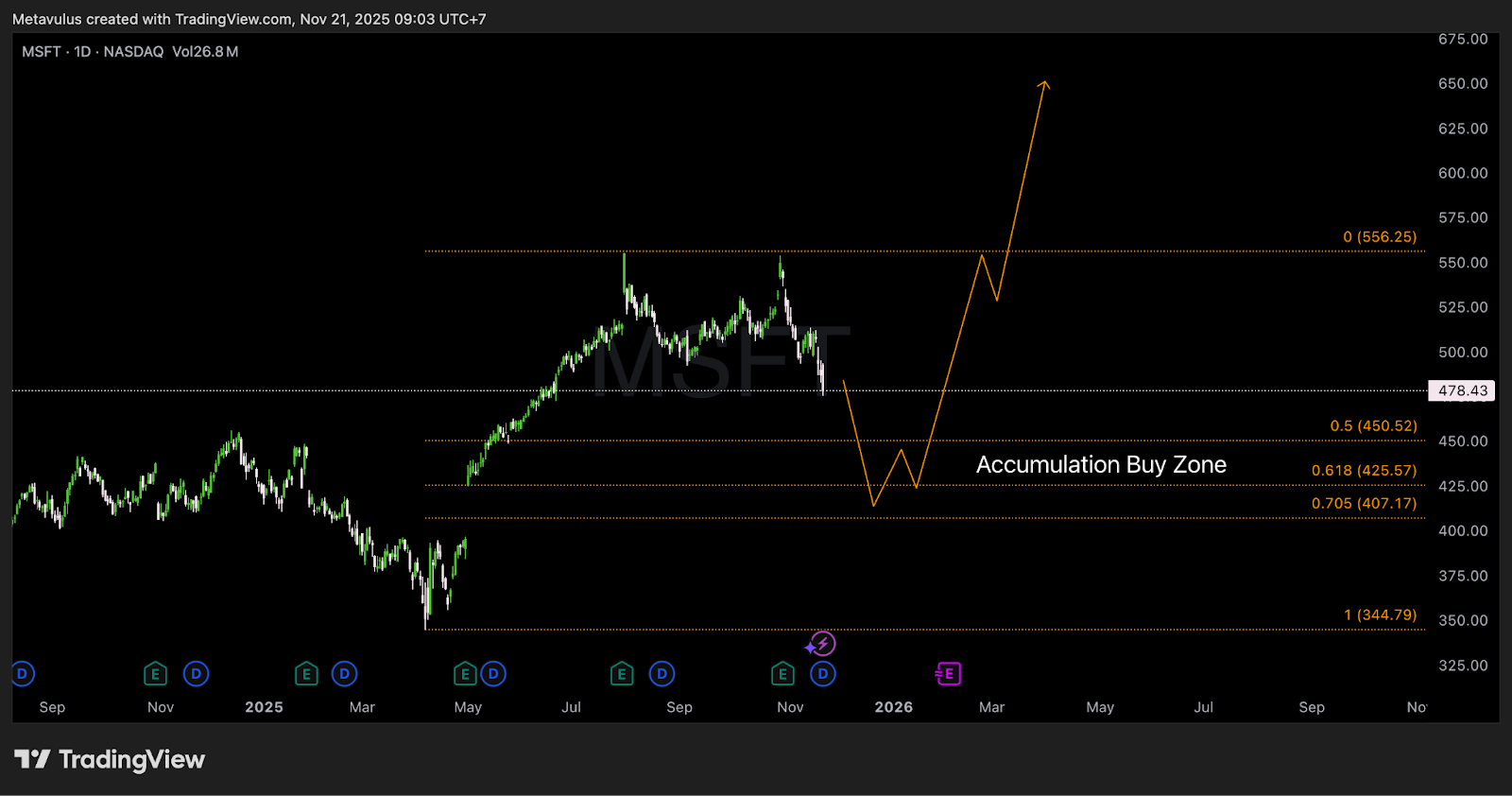

Current Price: ~US$478.43

Key Levels

Upside / Resistance

- 556.25 → prior swing high / Fib extension; first big upside target

- Above that = price discovery; 600–650 possible if AI mania resumes

Support & Fib Levels (Potential Buy Area)

- 450.52 (0.5 Fib) → first strong support

- 425.57 (0.618 Fib)

- 407.17 (0.705 Fib)

Accumulation Buy Zone

On your chart, the buy zone is mapped roughly around:

- Top of zone: ~US$450

- Middle: ~US$425–420

- Bottom: ~US$407

This cluster lines up with:

- 0.5–0.705 Fib retracement of the entire 2025 rally

- Prior consolidation area before the last leg higher

- Logical “value zone” for DCA in a mega-cap compounder

Invalidation

- Weekly close < US$400 → breaks 0.705 Fib + key structure → signals deeper re-rating risk; wait for new base around 360–345 (1.0 Fib / prior range)

Trading Setup

DCA Plan (Long-Term Investor, 3–5+ Years)

Target: build size only in/near Accumulation Buy Zone, not at ATH.

Example sizing:

- US$450–430: 35% of intended position

- US$430–410: 40% (core accumulation)

- US$410–390: 25% (flush bids if market pukes)

Approx full-fill average cost: US$420–435

Swing Trading Setup

- Entry 1: partial on reclaim of 450 after a dip (confirmation bounce)

- Entry 2: add in 430–415 zone if price holds daily support

- Stop (swing):

- Hard stop: daily close < 400, or

- More conservative: weekly close < 390

- Targets:

- TP1: 510–520 (prior range mid)

- TP2: 550–560 (previous major high / 556 Fib area)

- Stretch: 600+ if AI mania + multiple expansion return

Why The Thesis Works (Pillars)

Productivity & Business Processes = Cashflow Engine

- This segment (Office, Teams, Dynamics, LinkedIn) is:

- Growing ~16% YoY in revenue

- Expanding gross & operating profit at ~20% YoY

- Drivers:

- M365 E5 upgrades → higher ARPU

- Copilot add-ons → incremental high-margin AI upsell

- LinkedIn +10% YoY → employment & ad engine still solid

This is a sticky, mission-critical SaaS layer for global enterprises. Churn is near-zero; pricing power is real.

Intelligent Cloud / Azure = The Crown Jewel

- ~40% of total revenue but an even bigger share of future value

- Segment +28% YoY; Azure +40% YoY

- Management: demand in Azure AI “again exceeded supply” despite capacity addition

This is what justifies a premium P/E:

- Secular cloud + AI tailwinds

- Deep integration across Microsoft stack (Office, Windows, GitHub, Dynamics)

- Recurring, large-contract, enterprise-grade revenue

If Azure keeps compounding near 20%+ for years, EPS growth supports a 30x multiple.

Scale & Execution Offset Competitive Pressure (Partially)

Yes, competition is real:

- Google: Gemini 3, Docs/Sheets, Google Cloud

- Amazon: AWS still cloud leader in many verticals

- Others: Open-source LLMs, niche SaaS players

But Microsoft has:

- Distribution across every enterprise IT stack

- Tight bundling (Office + Teams + Copilot + Azure)

- Ability to subsidize AI features via huge existing cashflows

So while competitive risk is non-trivial, MSFT’s execution history + balance sheet gives it room to fight and still compound.

Balance Sheet & Cash Machine

- Market cap ~US$3.6T but also:

- Net cash fortress

- Robust FCF to fund:

- AI capex

- Dividends

- Buybacks

- M&A (e.g., Activision)

EPS can still grow high-teens over a cycle, bringing the forward P/E down organically if price stabilizes.

Valuation & Scenarios

(high-level, not a full DCF)

Current context:

- Forward P/E ≈ 30x

- YoY revenue growth: ~15–16%

- AI / cloud expected to drive above-GDP EPS compounding

Base Case (12–24 Months)

- Productivity & Cloud stay strong; Azure growth moderates toward high-20s

- More Personal Computing flat-to-low growth, no disaster

- Competition from Google/Amazon intense but not fatal

- Market keeps MSFT in 27–32x EPS range

🎯 Price range: US$520–560 → upside ~10–17% from current levels plus dividend

Bull Case (AI Mania 2.0)

- Azure continues 30–35%+ growth

- Copilot and AI subscriptions unlock new high-margin revenue streams

- Market assigns 35x+ multiple again

🎯 Price range: US$600–650+

Bear Case

- Windows & Xbox underperform more sharply than expected

- Valve/Apple/Sony erode gaming & PC OS moat faster than assumed

- Enterprise AI budgets normalize; Azure growth slows sharply

- Market re-rates mega-caps → P/E compresses to low-20s

🎯 Drawdown zone: US$380–400, with panic spikes possible to 350–360 (your 1.0 Fib around 344.79)

This is where DCA at scale becomes extremely attractive.

Risks

Key things to monitor:

- Xbox + Windows structural risk

- Activision deal must deliver real ecosystem value

- Valve’s SteamOS + new console, Apple & Sony pressure could weaken Xbox/Windows positioning in gaming

- AI & Cloud Competition

- Google Gemini gaining share vs OpenAI

- AWS and Google Cloud fighting aggressively on pricing & workloads → could cap Azure margins or growth.

- Regulatory / Anti-trust

- Big Tech remains a core target for US & EU regulators

- AI/data rules could slow certain monetization paths.

- Valuation Risk

- At ~30x earnings, any slowdown in Cloud/AI narrative could trigger multiple compression.

These don’t kill the long-term MSFT story, but they can hurt 1–2 year returns if bought at bad levels.

Conclusion

Microsoft remains:

- A top-tier compounder

- With world-class Productivity & Cloud engines

- Massive FCF & fortress balance sheet

- Real optionality in AI & Copilot

But:

- More Personal Computing (Windows/Xbox) is structurally less certain

- Competition in AI/cloud is heating up

- Valuation already prices in a lot of success

So the play is not blind diamond hands at any price, but:

Cautious accumulation on dips into your Accumulation Buy Zone, with expectations grounded, not euphoric.

Verdict: CAUTIOUS BUY

- Accumulate US$450 → 410

- Respect invalidation below US$400

- Aim for US$550+ over the next cycle, with upside to US$600+ if AI tailwinds stay extreme.

Disclaimer: Gotrade is the trading name of Gotrade Securities Inc., registered with and supervised by the Labuan Financial Services Authority (LFSA). This content is for educational purposes only and does not constitute financial advice. Always do your own research (DYOR) before investing.