The JEPI vs JEPQ debate has become one of the most common questions among income investors in 2026. Both are covered call ETFs from JPMorgan, both pay monthly distributions, and both charge the same expense ratio.

Yet they target very different stock universes and produce very different outcomes for your portfolio. Picking the wrong one can cost you growth or income depending on your goals.

This guide compares JEPI and JEPQ on the four dimensions that actually matter: yield, holdings, tax treatment, and portfolio fit.

How Covered Call ETFs Generate Income

A covered call ETF holds a basket of stocks and sells call options against those positions. The premium collected from selling those options becomes the bulk of the monthly distribution.

This strategy trades upside for income. When markets rally hard, the fund caps its gains because the calls get exercised. When markets stay flat or drift lower, the option premiums cushion returns.

Why investors choose this strategy

Retirees and income-focused investors use these funds to convert equity exposure into a steady cash stream. Yields above 8% are common, paid monthly, on a portfolio of large US stocks.

Traditional dividend funds rarely match those numbers without taking on credit risk or sector concentration in REITs and utilities.

The structural trade-off

You give up roughly half of strong bull-market returns. In exchange, you get income that does not depend on dividends alone, plus lower volatility than holding the underlying stocks outright.

That trade-off is the core question every income investor needs to answer before buying either fund.

JEPI: S&P 500 Defensive Tilt

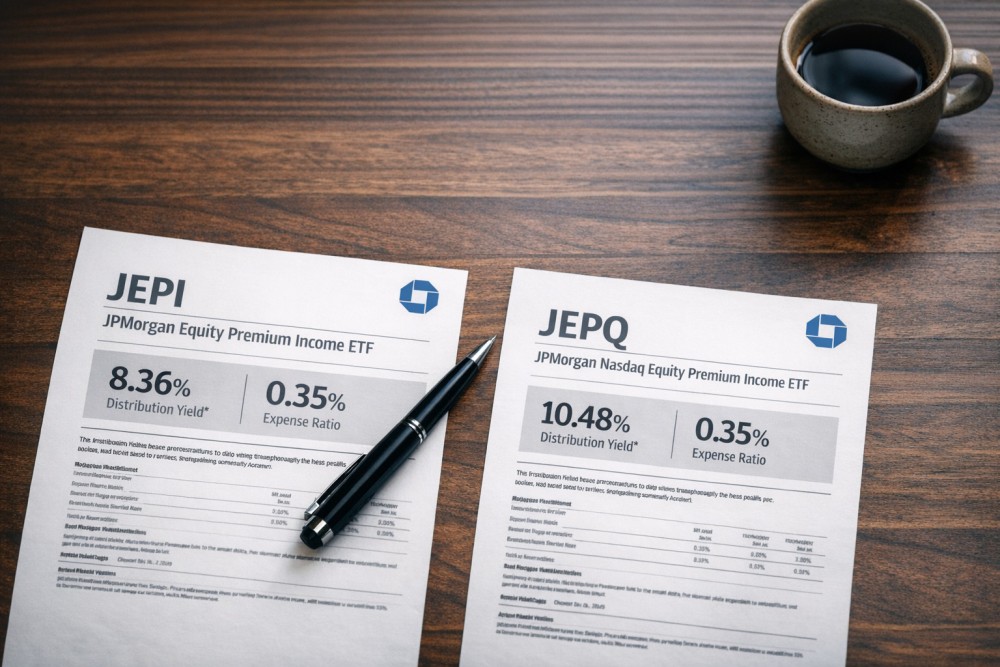

JEPI launched in May 2020 and now manages around $45 billion in assets. According to StockAnalysis, the fund yields 8.36% with a 0.35% expense ratio.

The fund holds about 123 stocks selected for low volatility and quality. Top positions are spread across sectors and individual names, with no holding above 1.8% of the portfolio.

Holdings concentration

The top five positions are Amazon, NVIDIA, Ross Stores, NextEra Energy, and Alphabet. Each sits between 1.66% and 1.74%, which keeps single-stock risk low.

What this means for your portfolio

JEPI behaves like a diversified equity fund with an income overlay. It tends to lose less in downturns than the S&P 500 and lag during sharp rallies.

For investors looking to manage market correction risk, that defensive profile is the main appeal of the fund.

JEPQ: Nasdaq 100 Tech Heavy Tilt

JEPQ launched in May 2022 and has scaled to about $37 billion in assets. The fund tracks Nasdaq 100 exposure with the same covered call overlay.

According to StockAnalysis, JEPQ yields 10.48% with a 0.35% expense ratio. The higher yield comes from richer option premiums on volatile tech names.

Holdings concentration

JEPQ is heavily concentrated in mega-cap tech. NVIDIA alone represents 8.37% of the fund, Apple 6.34%, and Alphabet 5.77%. The top ten holdings make up over 44% of assets.

What this means for your portfolio

JEPQ delivers more income but more risk. When tech sells off, the fund drops harder than JEPI. When tech rallies, it captures more upside before the calls cap returns. It is not a defensive holding.

Side-by-side comparison

| Metric | JEPI | JEPQ |

|---|

| Underlying universe | S&P 500 | Nasdaq 100 |

| Yield | 8.36% | 10.48% |

| Expense ratio | 0.35% | 0.35% |

| AUM | $45.0B | $37.2B |

| Top holding weight | 1.74% | 8.37% |

| Distribution | Monthly | Monthly |

Want to add a covered call ETF to your watchlist? Open a Gotrade account and start with fractional shares from $1, with zero commission on US stocks.

Tax Treatment and Distribution Mechanics

Covered call ETF distributions are not pure dividends. A meaningful portion is classified as ordinary income or short-term capital gains, depending on how the option premiums are realized.

This matters in taxable accounts. The high yield can lose more to tax drag than a qualified dividend ETF like SCHD or VYM, which compare a different tax profile in our starter portfolio guide.

Tax-advantaged accounts

JEPI and JEPQ work best inside an IRA or 401(k), where the ordinary-income classification does not matter. Reinvested distributions compound tax-free until withdrawal, which boosts long-run total return.

Taxable account considerations

If you hold either fund in a taxable brokerage, expect distributions to be taxed at your ordinary rate. Many investors run a simple analysis framework on after-tax yield before allocating capital between the two funds.

Conclusion

JEPI and JEPQ solve different problems. JEPI is the defensive income holding for investors who want steadier returns and lower drawdowns from S&P 500 exposure. JEPQ is the higher-octane choice for those willing to accept tech concentration in exchange for a 10%-plus yield.

Neither replaces a growth allocation. Both work as a complement to dividend ETFs like SCHD for diversified income exposure. Place them in tax-advantaged accounts when possible to keep more of the yield.

Ready to start building income exposure? Open a Gotrade account and add JEPI or JEPQ to your portfolio with fractional shares from $1 on US stocks.

FAQ

Is JEPQ riskier than JEPI?

Yes, JEPQ holds concentrated mega-cap tech and falls harder in tech-led drawdowns than JEPI's broader S&P 500 basket.

Can you hold both JEPI and JEPQ?

Yes, many investors blend them to balance defensive income from JEPI with higher-yield tech exposure from JEPQ.

Are JEPI and JEPQ distributions qualified dividends?

No, a meaningful portion is taxed as ordinary income, so both funds work best in tax-advantaged accounts.

Do covered call ETFs cap upside?

Yes, the fund sells call options that limit gains during sharp rallies in exchange for the premium income.