More Personal Computing flat-to-low growth, no disaster

Competition from Google/Amazon intense but not fatal

Market keeps MSFT in 27–32x EPS range

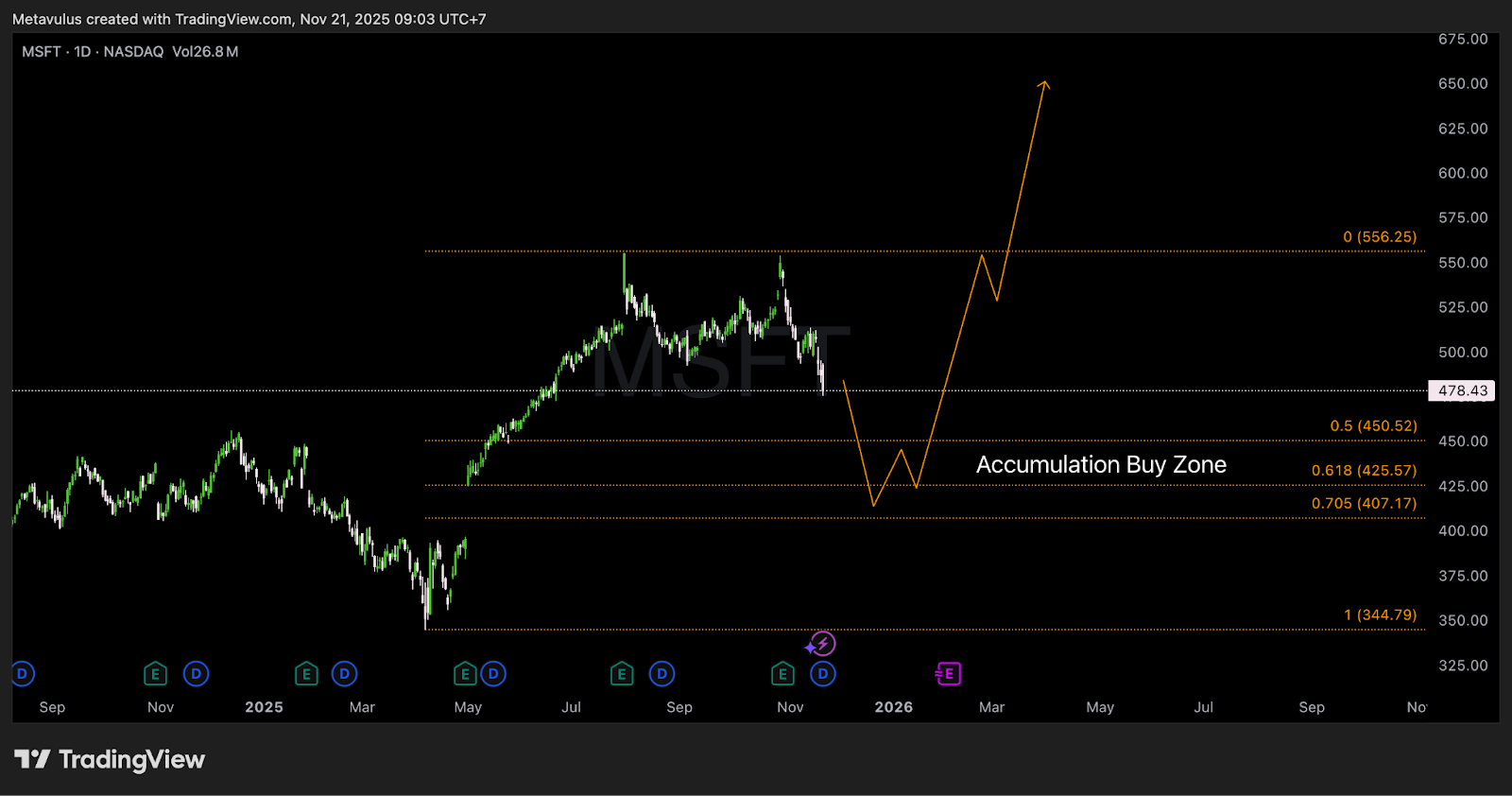

🎯 Price range:US$520–560 → upside ~10–17% from current levels plus dividend

Bull Case (AI Mania 2.0)

Azure continues 30–35%+ growth

Copilot and AI subscriptions unlock new high-margin revenue streams

Market assigns 35x+ multiple again

🎯 Price range:US$600–650+

Bear Case

Windows & Xbox underperform more sharply than expected

Valve/Apple/Sony erode gaming & PC OS moat faster than assumed

Enterprise AI budgets normalize; Azure growth slows sharply

Market re-rates mega-caps → P/E compresses to low-20s

🎯 Drawdown zone: US$380–400, with panic spikes possible to 350–360 (your 1.0 Fib around 344.79)

This is where DCA at scale becomes extremely attractive.

Risks

Key things to monitor:

Xbox + Windows structural risk

Activision deal must deliver real ecosystem value

Valve’s SteamOS + new console, Apple & Sony pressure could weaken Xbox/Windows positioning in gaming

AI & Cloud Competition

Google Gemini gaining share vs OpenAI

AWS and Google Cloud fighting aggressively on pricing & workloads → could cap Azure margins or growth.

Regulatory / Anti-trust

Big Tech remains a core target for US & EU regulators

AI/data rules could slow certain monetization paths.

Valuation Risk

At ~30x earnings, any slowdown in Cloud/AI narrative could trigger multiple compression.

These don’t kill the long-term MSFT story, but they can hurt 1–2 year returns if bought at bad levels.

Conclusion

Microsoft remains:

A top-tier compounder

With world-class Productivity & Cloud engines

Massive FCF & fortress balance sheet

Real optionality in AI & Copilot

But:

More Personal Computing (Windows/Xbox) is structurally less certain

Competition in AI/cloud is heating up

Valuation already prices in a lot of success

So the play is not blind diamond hands at any price, but:

Cautious accumulation on dips into your Accumulation Buy Zone, with expectations grounded, not euphoric.

Verdict: CAUTIOUS BUY

Accumulate US$450 → 410

Respect invalidation below US$400

Aim for US$550+ over the next cycle, with upside to US$600+ if AI tailwinds stay extreme.

Disclaimer: Gotrade is the trading name of Gotrade Securities Inc., registered with and supervised by the Labuan Financial Services Authority (LFSA). This content is for educational purposes only and does not constitute financial advice. Always do your own research (DYOR) before investing.