Altria (NYSE: MO) just gave income investors exactly what they want: more yield at cheaper prices. After a post-earnings sell-off on a tiny revenue miss, the underlying story is still intact:

Q3 2025 revenue (ex-excise) US$5.25B (-1.6% YoY) vs Street US$5.31B; adj. EPS US$1.45 (+5% YoY), in line with consensus.

FY25 EPS guide nudged up to US$5.41 (+4.2% YoY), slightly below Street’s US$5.44, enough to trigger a sentiment sell-off.

But: gross margin ~72.5% and operating company margin ~63.2% continue to expand vs 2019, proving strong pricing power and scale even as volumes fall.

Dividend King: 60th dividend increase in 56 years; quarterly dividend US$1.06/share, ~7% forward yield at current price.

Balance sheet healthier: net debt ~US$22.2B, net-debt/EBITDA down to ~1.8x from 2.3x in 2019.

Management continues to retire shares (-9.9% since 2019) while funding dividends and deleveraging.

Valuation: ~10.7x forward P/E and ~9.6x EV/EBITDA, at a discount to global tobacco peers.

Rating: BUY

Classic “boring compounding” dividend play; current pullback looks like a clean add / initiate zone for income and value investors.

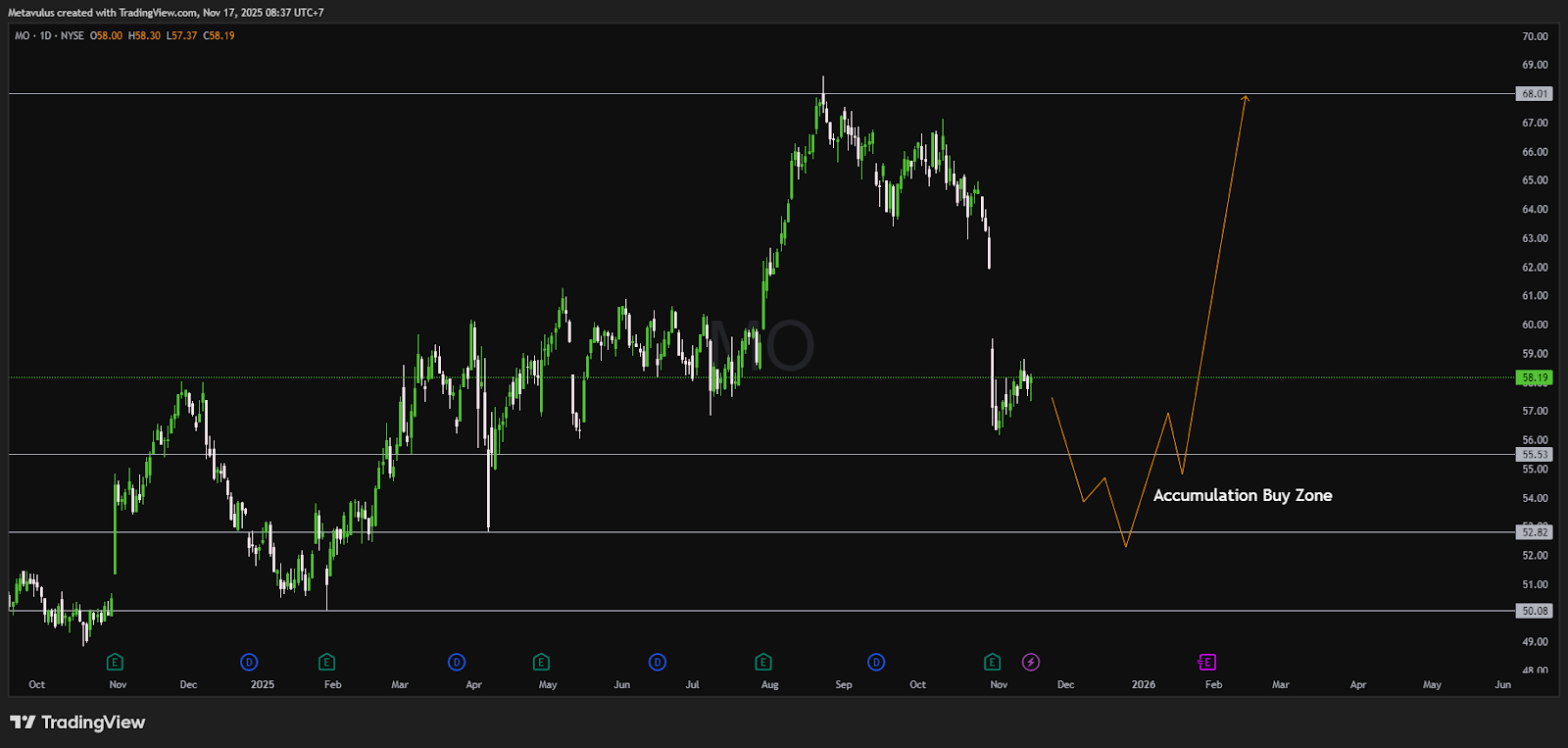

Technical Analysis

(based on attached Daily chart)

Current Price: ~US$58.19

Key Levels:

First Support:US$55.53, prior range low / likely first bounce area.

Accumulation Buy Zone:

US$52.82 – 50.08 → multi-year support band highlighted on chart.

Major Resistance / Target:

US$68.01 → prior swing high / range top.

Invalidation:

Weekly close below US$50.08 → breaks long-term support band; would reassess thesis / wait for fresh structure.

MO has retraced a good chunk of the Q2–Q3 2025 rally and is now consolidating in the high-50s after an earnings gap down. Base case: a choppy drift lower into US$53–50 completes a higher-timeframe “reload” before a swing back toward the high-60s. While price wanders, investors are paid ~7% in cash yearly.

Trading Setup

DCA Plan

Given this is a slow, income-type name, scaling in makes more sense than trying to nail the exact bottom:

30% size around US$56–55.5 (first support retest).

40% size around US$53–52.5 (top of accumulation zone).

30% size around US$51–50.2 (bottom of accumulation zone / “max fear”).

Risk Management

Swing / position traders:

Hard invalidation at weekly close < US$50.08.

Long-term income investors:

Focus more on dividend safety + leverage trends. Consider trimming if:

dividend coverage starts deteriorating materially, or

leverage spikes back toward 2.5–3x with no clear plan.

Take Profit Framework

TP1:US$63–64 → partial profit / move stop to breakeven for traders.

TP2:US$68.01 (prior high) → scale out further; leave a tail with trailing stop if yield still attractive and fundamentals intact.

Income Overlay

Sell cash-secured puts at US$55 / 52.5 (30–60 DTE) for investors happy to own lower.

Once assigned, sell covered calls at US$67.5–70 to juice yield on top of the ~7% dividend.

Regulatory / Litigation: Excise taxes, flavor bans, menthol rulings, and litigation are persistent overhangs for every tobacco name. Sudden adverse rulings could compress valuation and pressure cash flows.

NJOY / Reduced-Risk Products: Ongoing patent disputes and the challenge of executing in vaping / RRPs could cap growth if MO lags more innovative peers.

Volume Decline Acceleration: If U.S. cigarette declines accelerate beyond pricing power, margin expansion story may stall.

ESG & Multiple Compression: Structural ESG headwinds can keep valuation depressed, meaning investors may rely more on yield than price appreciation.

Conclusion

Altria is doing what a mature tobacco blue chip is supposed to do:

Convert a shrinking-but-sticky franchise into high, steady cash flow,

Pay out a large chunk as a dependable, rising dividend,

Gradually reduce share count and leverage,

And trade at a multiple that bakes in pessimism.

The market’s reaction to a tiny revenue miss and slightly conservative EPS guide looks more like noise than a thesis breaker. For investors seeking high, sustainable income with a reasonable chance of mid-single-digit EPS growth, MO at current prices is attractive.

Verdict: BUY.

Accumulate between US$56–50, respect US$50 as structural line in the sand, and let the 7% yield + slow compounding do the heavy lifting over the next 3–5 years.

Disclaimer

Gotrade is the trading name of Gotrade Securities Inc., registered with and supervised by the Labuan Financial Services Authority (LFSA). This content is for educational purposes only and does not constitute financial advice. Always do your own research (DYOR) before investing.