Amplitude (NASDAQ: AMPL) is a classic “growth at a reasonable price” setup: fundamentals are quietly improving, but the market is still pricing it like a broken IPO story.

Since IPO highs above US$80 in 2021, AMPL has been crushed, but Q3’25 marked a clear fundamental inflection:

Revenue +18% YoY (acceleration vs Q2’s +14%).

Net-new ARR US$12M, ARR +16% YoY to US$347M.

RPO (backlog) +37% YoY, with contract duration rising from 19 → ~22 months.

FY25 revenue guide raised to US$340.8–342.8M (+13.9–14.5% YoY) with pro-forma operating margin ~breakeven to slightly positive.

FY26 Street revenue ~US$390.7M (+14% YoY). At today’s price just above US$10:

EV/FY25 sales ≈ 3.3x

EV/FY26 sales ≈ 2.9x → Well below many 13–15% growth SaaS peers trading at 4.5–6x.

Balance sheet is bulletproof: ~US$267M cash, zero debt, positive FCF (~US$13.3M, 4.9% margin 9M’25).

AI is accelerating app creation and experimentation → more product teams need deep analytics on user journeys, where AMPL is a top pure-play.

Thesis: you’re paying a “broken IPO” multiple for a business that is quietly re-accelerating, lengthening contracts, and sitting in the slipstream of the AI app wave.

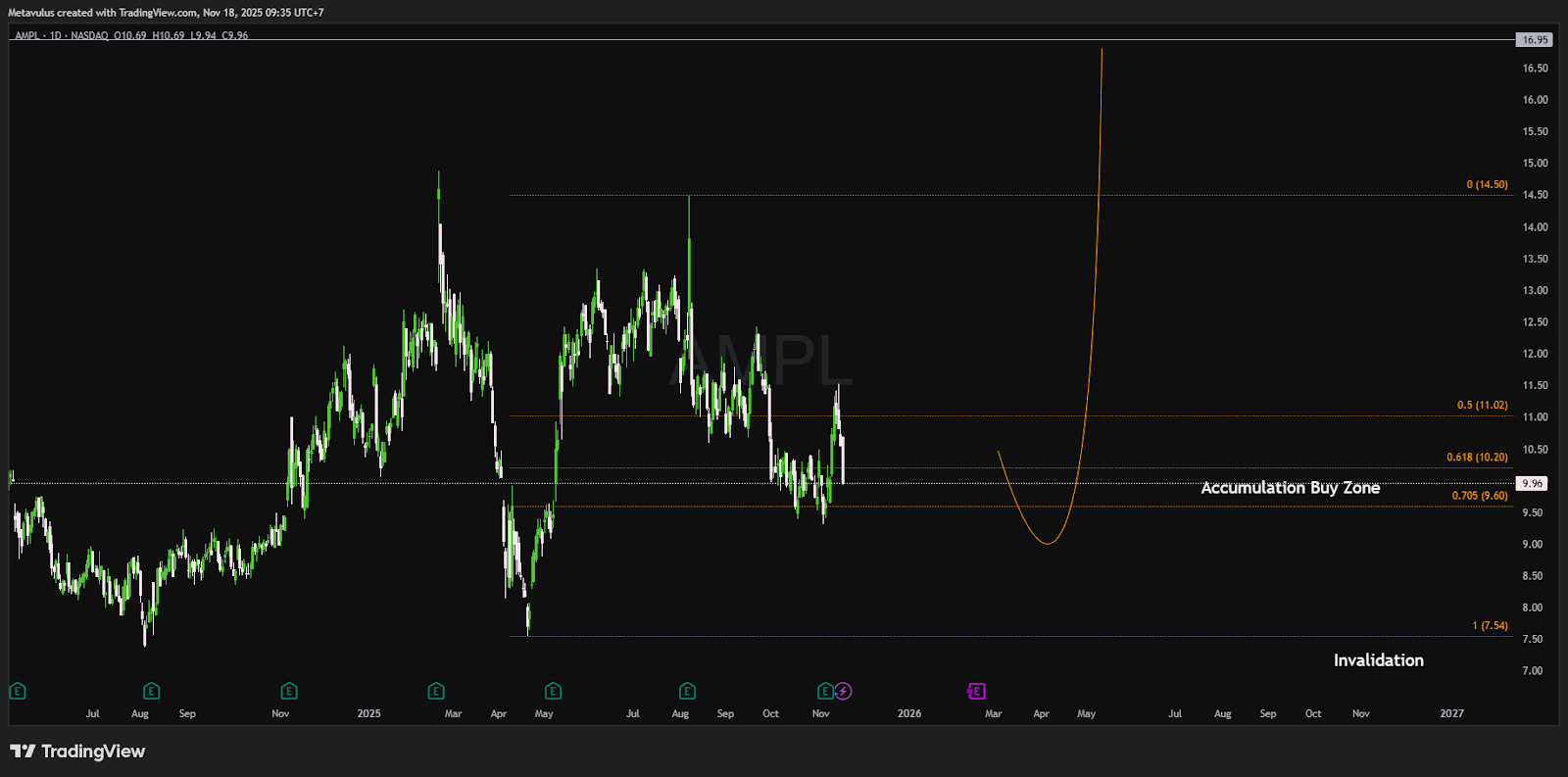

AMPL has already sold off hard and is now oscillating around the 0.618–0.705 retracement band, a classic spot where smart money accumulates if the fundamental story is improving.

As long as price holds above US$9.60 (ideally well above US$7.54), the risk/reward skew favors rotation back towards US$11–14, and in a full rerating scenario, US$16+.

Trading Setup

DCA Plan (Investor Focus, 12–24 Month Horizon)

Using your buy zone and fibs:

40% size at US$10.20–9.90

35% size at US$9.90–9.60 (bottom of Accumulation Zone)

AI wave = more apps, more experiments, more A/B tests → more need to measure product behaviour. AMPL is positioned as a specialist in that analytics layer.

4️⃣ Financial Discipline & Balance Sheet Strength

Pro-forma operating margin in Q3 ~0.6% (down YoY as they re-lean into growth).

Yet FCF is positive: US$13.3M (4.9% margin) in the first 9 months of FY25, slightly improving YoY.

Balance sheet: >US$250M net cash, zero debt.

AMPL can afford to prioritize growth and enterprise GTM without jeopardizing solvency or resorting to punitive dilutive financing.

Valuation & Scenarios (High-Level)

Assumptions (rough):

FY25–26 revenue growth ≈ 14–16%, then gradually moderates.

Long-term FCF margin can reach 15–20% if scale and efficiency continue.

Base Case (3–5 Years)

Revenue keeps compounding mid-teens; margins trend to low-teens.

Market re-rates AMPL from ~3x → ~4.5x FY26–27 sales as the turnaround is “obvious”.

Total return from current levels: ~40–70% over 3–4 years → mid-teens CAGR.

Bull Case

Growth sustains high-teens as AI app wave drives more demand.

Net retention rises into 107–110%+, RPO growth stays strong, AMPL becomes a “must-have” analytics layer narrative.

Market puts AMPL on 5.5–6x sales with improving margins.

Multi-bagger potential over 5 years (2–3x from today).

Bear Case

Competition intensifies, growth slips back to high-single digits.

RPO and contract duration flatten; AMPL loses share to cheaper/ bundled alternatives.

Market keeps multiple depressed around 2–3x sales. Stock chops sideways or drifts lower.

Even in the bear case, strong net cash and positive FCF limit true downside risk versus more leveraged SaaS names.

Key Risks

Competitive Crowd: Product analytics is a busy space; if Mixpanel, Heap, GA4, or new AI-native tools out-execute, AMPL’s growth can re-slow.

Macro & IT Budgets: Renewed SaaS derating or tighter marketing/product budgets could delay re-rating and compress multiples again

Execution: Pushing upmarket to enterprise requires consistent GTM discipline. Missteps could hurt win-rates and retention.

Valuation Overhang: The memory of the US$80 IPO peak may psychologically cap how aggressive some funds are willing to be, even as fundamentals improve.

Conclusion

Amplitude is not the hyper-growth rocket of 2021 anymore, but that’s exactly why the risk/reward is attractive now:

Growth has stabilized and is re-accelerating.

Backlog and contract duration are improving sharply.

Balance sheet is clean, FCF is positive, and valuation is cheap vs peers.

If you believe:

AI will create more digital products,

Those products will need better measurement of user behaviour, and

AMPL can remain one of the go-to analytics platforms for serious product teams,

…then buying here around US$10 while the market is still ignoring the turnaround is a rational, asymmetric bet.

Verdict: BUY. Accumulate in the US$10.20–9.60 zone, look for a 2026 re-rating towards US$14–17, and think in multi-year terms, not multi-week swings.

Disclaimer

Gotrade is the trading name of Gotrade Securities Inc., registered with and supervised by the Labuan Financial Services Authority (LFSA). This content is for educational purposes only and does not constitute financial advice. Always do your own research (DYOR) before investing.